November 28th, 2025

A practical guide for successful business owners looking to put excess cash to work.

If you're a successful business owner in Canada with cash sitting in your corporation, you're likely paying close to 50% tax on any passive investment income. But there's a better way, one that could reduce your tax rate to 0%.

At PE Gate, our mission is to help accredited investors and Canadian business owners benefit from private company investments. This guide walks you through the tax-efficient strategies we deploy with our portfolio companies and the investment frameworks that allow corporate investors to achieve 0% tax on their returns.

These insights were gleaned from a recent panel discussion hosted by PE Gate in partnership with Canadian Wealth Secrets and Gauvreau | Accounting Tax Law Advisory. Watch the full conversation on the PE Gate YouTube Channel, or continue reading for a detailed breakdown of the key takeaways.

To receive invitations to future live events in the GTA, you can sign up here.

The Foundation: Start with a Family Trust

If you operate a successful business, the first step in tax-efficient wealth building is establishing a family trust structure. This unlocks the Lifetime Capital Gains Exemption (LCGE) and provides critical asset protection.

The LCGE allows individuals to realize approximately $1.25 million in capital gains at nearly zero tax. Here's where the family trust becomes powerful: if you have a $5 million capital gain when you exit your business, you can spread that $1.25 million exemption across multiple family members. This means potentially sheltering the entire gain from tax.

This is an almost-zero tax outcome, one of the only truly tax-free mechanisms available to Canadian business owners.

Important considerations:

- The LCGE is available to individuals, not corporations

- Your company must be properly "purified" to qualify, meaning it holds primarily active assets with minimal passive investments

- Professional tax and legal advice is essential to ensure your specific situation qualifies

Additionally, using a family trust can allow multiple beneficiaries to use their LCGE, but there are strict CRA rules:

- Shares must be “qualified small business corporation shares” (QSBCS)

- The shares must meet the two-year holding and 90% active business property tests

- Simply using a family trust does not guarantee 0% tax on a $5M gain; the LCGE limit per individual is fixed ($1.25M in 2025), so full sheltering depends on number of eligible beneficiaries

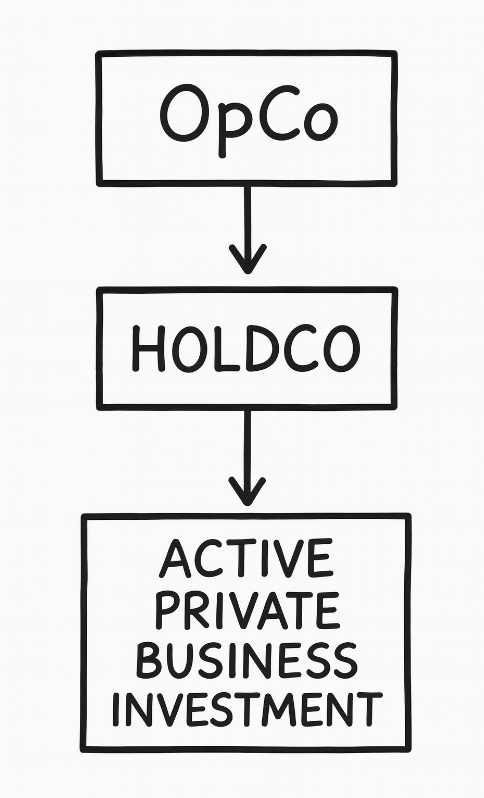

Keep Your Operating Company Lean and Active

While building your family trust structure, focus on keeping your operating company (OpCo) lean and active. This means maintaining your focus on active business operations rather than passive investments.

Think of it this way: when your business clears a million dollars this year, the government is essentially saying, "Don't take that out and buy a car. Reinvest it in your business, or invest in another active business." The government wants to reward you for keeping capital working in the real economy.

Avoid accumulating excess passive assets in your OpCo, which can:

- Trigger passive income tax at approximately 50%

- Jeopardize your LCGE eligibility

- Expose assets to operating risk

Move excess cash regularly to a separate holding company (HoldCo). This approach:

- Protects assets from business liabilities

- Preserves LCGE eligibility for your operating company

- Positions retained earnings for tax-efficient reinvestment

The principle is simple: passive investments (public markets, GICs) get taxed at approximately 50%. Active private businesses where you own more than 10% equity unlock preferential tax treatment.

The 0% Tax Opportunity: Investing in Active Businesses

Here's where the story gets interesting, and where PE Gate's primary focus comes in. When you invest in an active private business as a "connected corporation," dividends can flow at a 0% tax rate.

Why 0%? Under CRA rules, your HoldCo qualifies as a connected corporation when it owns:

- More than 10% of voting shares, AND

- More than 10% of equity value

This prevents double taxation. When you invest in an active private business, that business has already paid corporate tax on its profits (often around 12% for small businesses in Ontario). When it distributes dividends to your HoldCo, the government's position is clear: why would we tax you again on money that's already been taxed? That would be double taxation.

Here's how the math works on a $100,000 investment:

- Your initial return of capital ($100,000) comes back tax-free

- Ongoing dividends flow to your HoldCo at 0% tax

- If you eventually sell your position, 50% of your capital gain is taxable (only on the gain, not the principal)

How PE Gate Structures Deals for 0% Tax Treatment

PE Gate ensures corporate investors qualify as connected corporations by:

- Providing >10% equity ownership in each investment opportunity

- Issuing real, participating voting share classes to meet CRA requirements

- Structuring investments deal-by-deal, not through blind-pool funds, so investors maintain the connected corporation status

Because we limit corporate investors in every deal, each can hold meaningful equity (10%+) and receive real voting rights. This is highly unusual in private equity, where most funds structure investors as limited partners without the voting rights required for 0% dividend treatment.

PE Gate accepts both corporate and personal investment. The 0% dividend treatment on connected corporations requires investing through your HoldCo, while personal investment can be advantageous for utilizing your LCGE.

Investors must obtain their own tax advice to confirm personal eligibility.

Where Should You Invest: Personal or Corporate?

A common question: if you have money both personally and in a corporation, which should you use for private investments?

The simple answer: invest where the money currently is. Don't move money from a corporation to personal accounts (paying tax) just to get the LCGE benefit. However, there are strategic considerations:

For personal investment:

- If you haven't used your LCGE and are investing in a growth-oriented opportunity with a clear exit strategy, personal investment may make sense

- You can realize capital gains at nearly 0% tax up to the LCGE limit

For corporate investment:

- If the investment is a dividend-focused opportunity you plan to hold long-term, invest through your corporation

- Dividends flow to your HoldCo at 0% tax

- Capital is immediately redeployable without triggering personal tax

Matching investments to your strategy

The beauty of PE Gate's model is that different opportunities serve different goals:

Growth-oriented (better for personal/LCGE): Our pet services roll-up is a long-term acquisition and growth strategy with clear exit potential to U.S.-based private equity. During the growth phase, dividends are minimal as we continue to fundraise for acquisitions, but the eventual capital gain can be substantial—making it ideal for individuals looking to utilize their LCGE.

Dividend-focused (better for corporate): Our deal with Kingston Refractory takes a different approach. This established, stable business pays regular semi-annual dividends and operates on a very long-term hold strategy with employee ownership. It's perfect for corporate investors seeking 0% tax on ongoing income. Similarly, our Klimatrol investment is a co-investment with operators featuring employee ownership and a steady dividend play rather than an exit-focused strategy.

Each investment's goals, dividend policy, and exit strategy are disclosed in the offering memorandum, allowing you to choose opportunities that align with your tax structure and timeline.

Corporate-Owned Insurance: Accessing Retained Earnings When You Need To

Even with a strong corporate structure and tax-efficient investment strategy, many business owners eventually ask: how do I access my retained earnings personally without a large tax impact?

Corporate-owned life insurance provides a solution. When integrated with your investment strategy, it can:

- Provide tax-efficient liquidity

- Enable borrowing against the policy during life

- Transfer retained earnings out of a corporation at a reduced tax rate

- Support estate and succession planning

This creates optionality without triggering immediate tax. Here's where it becomes particularly powerful: when your HoldCo receives 0% tax dividends from active business investments, those dividends can fund corporate-owned insurance premiums. The policy's cash value grows in a tax-sheltered environment, and Immediate Financing Arrangements (IFAs) can provide access to capital without triggering personal tax.

While these strategies can be costly and complex, they work best when you have substantial retained earnings and want to maintain flexibility for future personal access to capital.

Putting It All Together: A Practical Wealth-Building Framework

The strategy is straightforward: keep capital in your corporate ecosystem, prioritize active business investments where dividends flow at 0% tax, and let it compound before personal tax applies. For successful business owners, the path to tax-efficient wealth building follows this sequence:

- Establish your family trust structure to maximize LCGE benefits at exit

- Keep your operating company lean and focused on active business assets

- Move excess cash to a HoldCo to protect assets and create flexibility

- Invest in active private businesses where you own >10% in votes and value to unlock 0% tax on dividends

- Match investments to your structure: growth plays for personal capital (utilizing LCGE), dividend plays for corporate capital

- Use those tax-free corporate dividends to fund corporate-owned insurance strategies, creating a compounding, tax-advantaged wealth engine inside the corporation

When these components work together, you create a powerful and integrated structure:

- Your HoldCo receives 0% tax dividends from active business investments

- Those dividends fund corporate-owned insurance premiums

- The policy's cash value grows in a tax-sheltered environment

- Immediate Financing Arrangements (IFAs) can provide access to capital without triggering personal tax, allowing retained earnings to remain invested and compounding inside the corporation

The difference between 50% tax and 0% tax on investment returns compounds dramatically over time. For business owners with $500,000+ in retained earnings, understanding and implementing these strategies can fundamentally transform your wealth-building trajectory.

Ready to Put Your Retained Earnings to Work?

If you're a business owner with excess cash in your corporation, we'd welcome the opportunity to discuss how PE Gate's active business investments could fit your wealth-building strategy. Whether you're looking to deploy retained earnings at 0% tax or exploring a partial or full exit from your own business, our team is here to help.

Reach out to discuss investment opportunities or explore partnership options for your business exit.

And if you're wondering whether it might be time to transition from your current business, read our article: You've Built Something Great: 5 Signs It's Time for What's Next.

Disclaimer

This material is provided for informational purposes only and does not constitute investment, legal, or tax advice. Tax rules are complex and subject to change, and every individual situation is unique. We strongly recommend that you consult your own qualified tax advisor before making any investment or tax-related decisions.

Prospective investors should consult their own tax and legal advisors to determine how these concepts may apply to their specific situation. Participation in private investments through PE Gate is limited to accredited and other qualified investors.